The hardware and bandwidth for this mirror is donated by dogado GmbH, the Webhosting and Full Service-Cloud Provider. Check out our Wordpress Tutorial.

If you wish to report a bug, or if you are interested in having us mirror your free-software or open-source project, please feel free to contact us at mirror[@]dogado.de.

Pierre Gaillard, Yannig Goude

![]()

opera useful?

![]()

opera is a R package that provides several algorithms to

perform robust online prediction of time series with the help of expert

advice. In this vignette, we provide an example of how to use the

package.

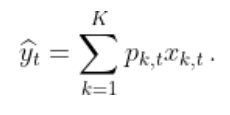

opera useful?Consider a sequence of real bounded observations y1, …, yn to be predicted step by step. Suppose that you have at your disposal a finite set of methods k = 1, …, K (henceforth referred to as experts) that provide you before each time step t = 1, …, n predictions xk, t of the next observation yt. You can form your prediction ŷt by using only the knowledge of the past observations y1, …, yt − 1 and past and current expert forecasts xk, 1, …, xk, t for k = 1, …, K. The package opera implements several algorithms of the online learning literature that form predictions ŷt by combining the expert forecasts according to their past performance. That is,

These algorithms come with finite time worst-case guarantees. The monograph of Cesa-Bianchi and Lugisi (2006) gives a complete introduction to the setting of prediction of arbitrary sequences with the help of expert advice.

The package opera provides three important functions:

mixture to build the algorithm object, predict

to make a prediction by using the algorithm, and oracle to

evaluate the performance of the experts and compare the performance of

the combining algorithm.

opera is now available on CRAN, so you can install it with:

install.packages("opera")You can also install the development version of opera with the package devtools:

install.packages("devtools")

devtools::install_github("dralliag/opera")You may be asked to install additional necessary packages. You can install the package vignette by setting the option: build_vignettes = TRUE.

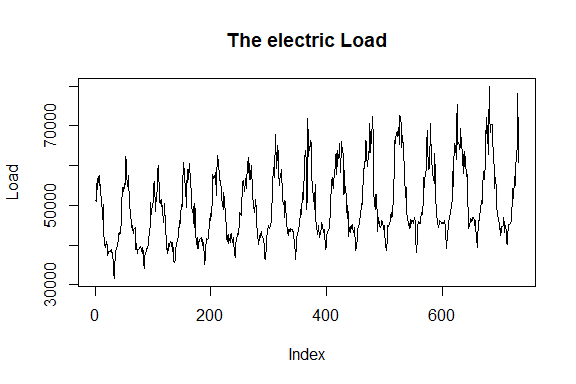

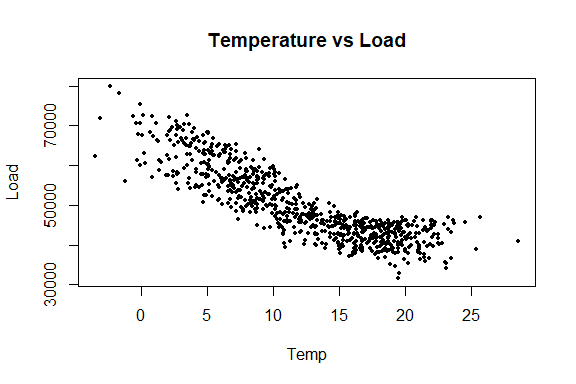

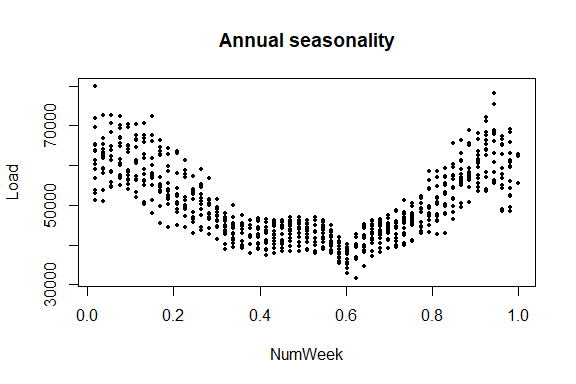

Here, we provide a concrete example on how to use the package. To do so, we consider an electricity forecasting data set that includes weekly observations of the French electric load together with several covariates: the temperature, calendar information, and industrial production indexes. The data set is provided by the French National Institute of Statistics and Economic Studies (Insee).

library(opera)

set.seed(1)First, we load the data and we cut it into two subsets: a training set used to build the experts (base forecasting methods) and a testing set (here the last two years) used to evaluate the performance and to run the combining algorithms.

data(electric_load)

attach(electric_load)

idx_data_test <- 620:nrow(electric_load)

data_train <- electric_load[-idx_data_test, ]

data_test <- electric_load[idx_data_test, ] The data is displayed in the following figures.

plot(Load, type = "l", main = "The electric Load")

plot(Temp, Load, pch = 16, cex = 0.5, main = "Temperature vs Load")

plot(NumWeek, Load, pch = 16, cex = 0.5, main = "Annual seasonality")

Here, we build three base forecasting methods to be combined later.

mgcv

package:library(mgcv)

gam.fit <- gam(Load ~ s(IPI) + s(Temp) + s(Time, k=3) +

s(Load1) + as.factor(NumWeek), data = data_train)

gam.forecast <- predict(gam.fit, newdata = data_test)# medium term model

medium.fit <- gam(Load ~ s(Time,k=3) + s(NumWeek) + s(Temp) + s(IPI), data = data_train)

electric_load$Medium <- c(predict(medium.fit), predict(medium.fit, newdata = data_test))

electric_load$Residuals <- electric_load$Load - electric_load$Medium

# autoregressive correction

ar.forecast <- numeric(length(idx_data_test))

for (i in seq(idx_data_test)) {

ar.fit <- ar(electric_load$Residuals[1:(idx_data_test[i] - 1)])

ar.forecast[i] <- as.numeric(predict(ar.fit)$pred) + electric_load$Medium[idx_data_test[i]]

}caret packagelibrary(caret)

gbm.fit <- train(Load ~ IPI + IPI_CVS + Temp + Temp1 + Time + Load1 + NumWeek, data = data_train, method = "gbm")

gbm.forecast <- predict(gbm.fit, newdata = data_test)Once the expert forecasts have been created (note that they can also be formed online), we build the matrix of expert and the time series to be predicted online

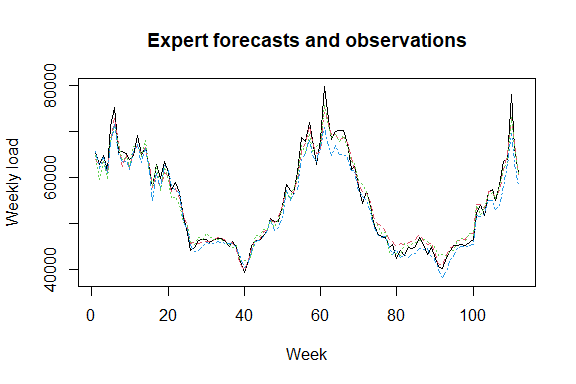

Y <- data_test$Load

X <- cbind(gam.forecast, ar.forecast, gbm.forecast)

matplot(cbind(Y, X), type = "l", col = 1:6, ylab = "Weekly load",

xlab = "Week", main = "Expert forecasts and observations")

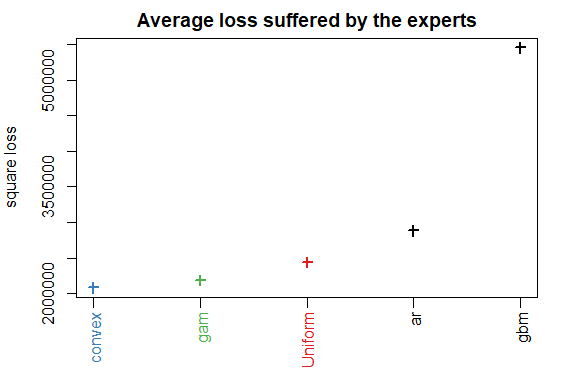

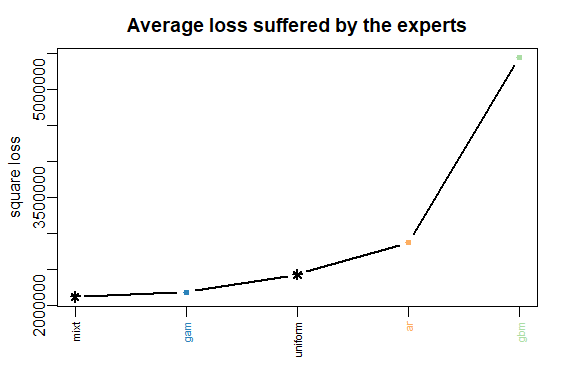

To evaluate the performance of the experts and see if the aggregation rules may perform well, you can look at the oracles (rules that are used only for analysis and cannot be design online).

oracle.convex <- oracle(Y = Y, experts = X, loss.type = "square", model = "convex")

print(oracle.convex)

plot(oracle.convex)

#> Call:

#> oracle.default(Y = Y, experts = X, model = "convex", loss.type = "square")

#>

#> Coefficients:

#> gam ar gbm

#> 0.719 0.201 0.0799

#>

#> rmse mape

#> Best expert oracle: 1480 0.0202

#> Uniform combination: 1560 0.0198

#> Best convex oracle: 1440 0.0193

The parameter loss.type defines the evaluation

criterion. It can be either the square loss, the percentage loss, the

absolute loss, or the pinball loss to perform quantile regression.

The parameter model defines the oracle to be calculated.

Here, we computed the best fixed convex combination of expert (i.e.,

with non-negative weights that sum to one).

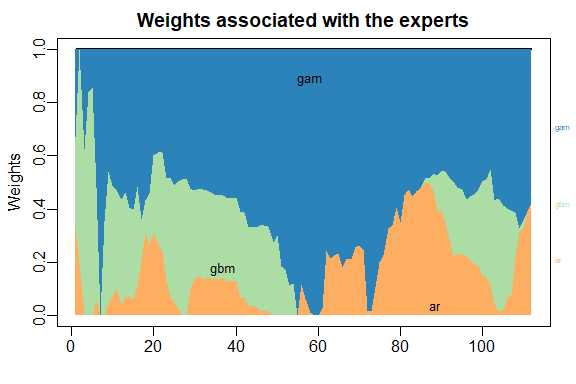

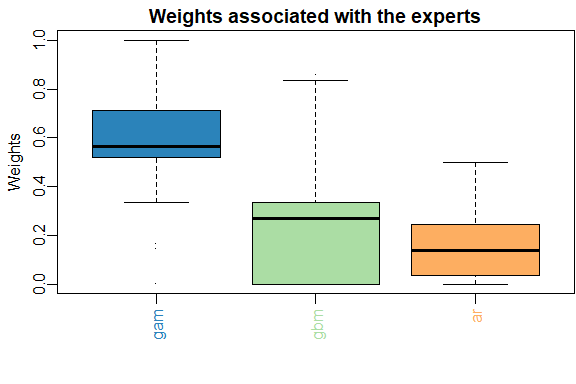

The first step consists in initializing the algorithm by defining the type of algorithm (Ridge regression, exponentially weighted average forecaster,…), the possible parameters, and the evaluation criterion. If no parameter is defined by the user, all parameters will be calibrated online by the algorithm. Bellow, we define the ML-Poly algorithm, evaluated by the square loss.

MLpol0 <- mixture(model = "MLpol", loss.type = "square")Then, you can perform online predictions by using the

predict method. At each time, step the aggregation rule

forms a new prediction and update the procedure.

MLpol <- MLpol0

for (i in 1:length(Y)) {

MLpol <- predict(MLpol, newexperts = X[i, ], newY = Y[i])

}The results can be displayed with method summary and

plot.

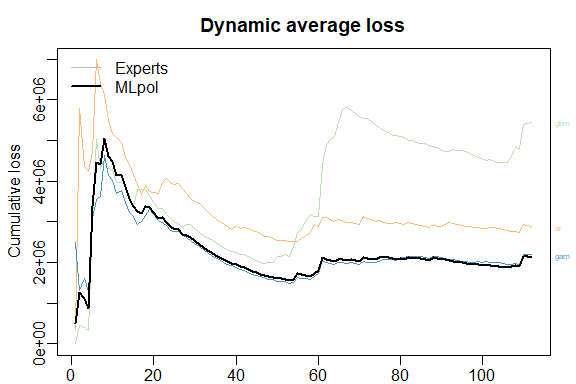

summary(MLpol)

#> Aggregation rule: MLpol

#> Loss function: squareloss

#> Gradient trick: TRUE

#> Coefficients:

#> gam ar gbm

#> 0.577 0.423 0

#>

#> Number of experts: 3

#> Number of observations: 112

#> Dimension of the data: 1

#>

#> rmse mape

#> MLpol 1460 0.0192

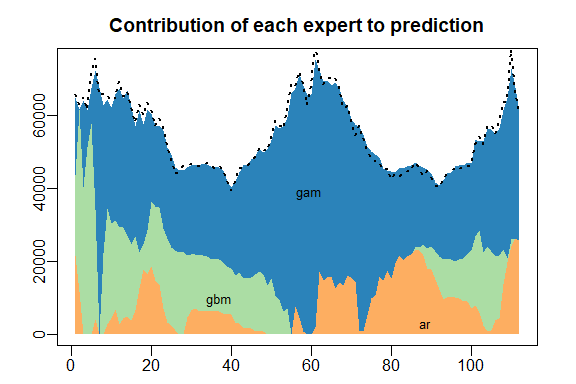

#> Uniform 1560 0.0198plot(MLpol)

The same results can be obtained more directly:

predict specifying

online = TRUE to perform online prediction.MLpol <- predict(MLpol0, newexpert = X, newY = Y, online = TRUE)MLpol <- mixture(Y = Y, experts = X, model = "MLpol", loss.type = "square")The vector of predictions formed by the mixture can be obtained through the output prediction.

predictions <- MLpol$predictionNote that these predictions were obtained sequentially by the algorithm by updating the model coefficients after each data. It is worth to emphasize that each observation is used to get the prediction of the next observations but not itself (nor past observations).

In real-world situations, predictions should be produced without

having access to the observed outputs. There are several solutions to

get them with opera.

Using the predict method with the arguments *

online = FALSE: the model coefficients are not updated

during the prediction. * type = response: the predictions

are returned and not an updated model.

newexperts <- X[1:3, ] # Experts forecasts to predict 3 new points

pred <- predict(MLpol, newexperts = newexperts, online = FALSE, type = 'response')#> [1] 64397.10 61317.41 63571.59The same result can be easily obtained by using the last model coefficients to perform the weighted average of the expert advice.

pred = newexperts %*% MLpol$coefficients#> [1] 64397.10 61317.41 63571.59In some situations, the aggregation model cannot be updated at each step due to an operational constraint. One must predict the time-series y1, …, yn block by block. For example, a weather website might want to make a daily forecast of the next day’s temperature at hourly intervals. This corresponds to block by block predictions of 24 observations.

Let’s say that in the above example, instead of making a weekly

prediction, we need to predict every four weeks, the consumption of the

next four weeks. Below we show two different ways to use the

opera package to do this.

Note that the outputs

y1, …, yn to be

predicted step by step can be d-dimensional in

opera. In this case, the argument Y provided

to the function mixture should be a matrix, where each line

corresponds to the output observed at time t; the argument

experts must be an array of dimension

T × d × K such that

experts[t,:,k] is the prediction made by expert k

at iteration t. These predictions of dimension d can

be used in various situations. For example, we might want to

simultaneously predict the electricity consumption of several countries

in the example above.

Another useful application of this feature is block by block prediction. Consider the above example of electricity consumption to be predicted every four weeks. This can be easily done by transforming the original time series into a 4 dimensional time series, where each row corresponds to the four weeks to predict after each update.

YBlock <- seriesToBlock(X = Y, d = 4)

XBlock <- seriesToBlock(X = X, d = 4)The four-week-by-four-week predictions can then be obtained by

directly using the mixture function as we did earlier.

MLpolBlock <- mixture(Y = YBlock, experts = XBlock, model = "MLpol", loss.type = "square")The predictions can finally be transformed back to a regular one

dimensional time-series by using the function

blockToSeries.

prediction <- blockToSeries(MLpolBlock$prediction)online = FALSE optionAnother equivalent solution is to use the online = FALSE

option in the predict function. The latter ensures that the model

coefficients are not updated between the next four weeks to

forecast.

MLpolBlock <- MLpol0

d = 4

n <- length(Y)/d

for (i in 0:(n-1)) {

idx <- 4*i + 1:4 # next four weeks to be predicted

MLpolBlock <- predict(MLpolBlock, newexperts = X[idx, ], newY = Y[idx], online = FALSE)

}As we see below, the coefficients are updated every four lines only.

#> [,1] [,2] [,3]

#> [1,] 0.3333333 0.3333333 0.3333333

#> [2,] 0.3333333 0.3333333 0.3333333

#> [3,] 0.3333333 0.3333333 0.3333333

#> [4,] 0.3333333 0.3333333 0.3333333

#> [5,] 0.1437215 0.0000000 0.8562785

#> [6,] 0.1437215 0.0000000 0.8562785These binaries (installable software) and packages are in development.

They may not be fully stable and should be used with caution. We make no claims about them.

Health stats visible at Monitor.