The hardware and bandwidth for this mirror is donated by dogado GmbH, the Webhosting and Full Service-Cloud Provider. Check out our Wordpress Tutorial.

If you wish to report a bug, or if you are interested in having us mirror your free-software or open-source project, please feel free to contact us at mirror[@]dogado.de.

![]()

![]()

![]()

![]()

![]()

hcinfer computes heteroskedasticity-consistent

covariance estimators and normal Wald inference for ordinary least

squares models. The currently implemented covariance matrix estimators

are listed below.

The table below is generated by hc_methods() and lists

the covariance matrix estimators currently implemented in

hcinfer.

| type | label | description | default_arguments |

|---|---|---|---|

| hc0 | HC0 | White heteroskedasticity-consistent estimator. | none |

| hc1 | HC1 | HC0 with degrees-of-freedom scaling. | none |

| hc2 | HC2 | Leverage-adjusted estimator with exponent 1. | none |

| hc3 | HC3 | Leverage-adjusted estimator with exponent 2. | none |

| hc4 | HC4 | Adaptive leverage correction by Cribari-Neto. | none |

| hc4m | HC4m | Modified HC4 correction by Cribari-Neto and da Silva. | none |

| hc5 | HC5 | High-leverage correction by Cribari-Neto, Souza, and Vasconcellos. | k = 0.7 |

| hc5m | HC5m | Modified HC5 correction by Li, Zhang, Zhang, and Wang. | k = 0.7, k1 = 1, k2 = 0, k3 = 1, gamma1 = 1, gamma2 = 1.5 |

| hcbeta | HCbeta | Beta-distribution leverage correction. | c1 = 7, c2 = 0.75, lower = 0.01, upper = 0.99 |

# Official CRAN installation of the package

install.packages("hcinfer")

# r-universe installation

install.packages('hcinfer', repos = c('https://prdm0.r-universe.dev', 'https://cloud.r-project.org'))

# Development version installation from GitHub

remotes::install_github("prdm0/hcinfer", force = TRUE)library(hcinfer)

schools <- PublicSchools

schools$income_scaled <- schools$income / 10000

schools$income_scaled_sq <- schools$income_scaled^2

fit <- lm(expenditure ~ income_scaled + income_scaled_sq, data = schools)

result <- hcinfer(fit)The default estimator is HCbeta. Use tests() and

confint() to extract the main inferential quantities as

tibbles.

tests(result)

#> # A tibble: 3 × 8

#> term estimate null_value std_error z_value p_value alpha reject

#> <chr> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl> <lgl>

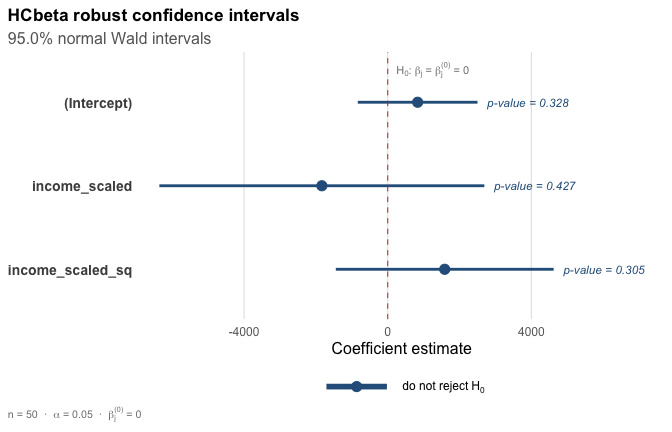

#> 1 (Intercept) 833. 0 851. 0.979 0.328 0.05 FALSE

#> 2 income_scaled -1834. 0 2309. -0.794 0.427 0.05 FALSE

#> 3 income_scaled_sq 1587. 0 1547. 1.03 0.305 0.05 FALSE

confint(result)

#> # A tibble: 3 × 4

#> term conf_low conf_high level

#> <chr> <dbl> <dbl> <dbl>

#> 1 (Intercept) -834. 2500. 0.95

#> 2 income_scaled -6359. 2691. 0.95

#> 3 income_scaled_sq -1446. 4620. 0.95The plot() method displays the robust confidence

intervals and marks the null value used in the tests.

plot(result)

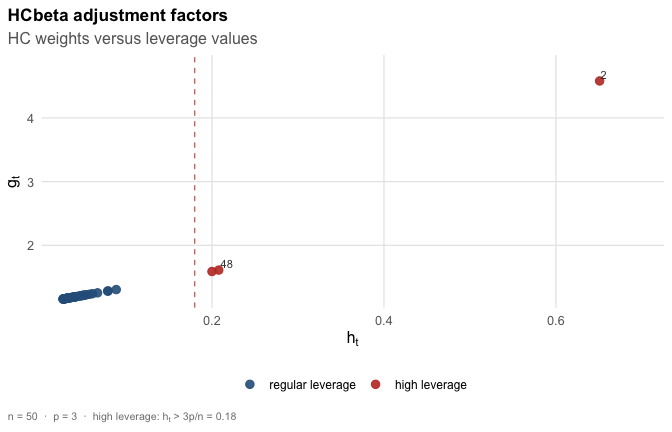

Use vcov_hc() when you only need the robust covariance

matrix and its diagnostics. The plot() method for this

object shows leverage values and HC adjustment factors.

cov_hcbeta <- vcov_hc(fit)

plot(cov_hcbeta)

hc_methods()

coef(result)

vcov(result)The most common workflow is:

fit <- lm(y ~ x1 + x2, data = data)

result <- hcinfer(fit, type = "hcbeta")

summary(result)

tests(result)

confint(result)

plot(result)Start with vignette("introduction", package = "hcinfer")

for a compact overview of the package API.

These binaries (installable software) and packages are in development.

They may not be fully stable and should be used with caution. We make no claims about them.

Health stats visible at Monitor.