The hardware and bandwidth for this mirror is donated by dogado GmbH, the Webhosting and Full Service-Cloud Provider. Check out our Wordpress Tutorial.

If you wish to report a bug, or if you are interested in having us mirror your free-software or open-source project, please feel free to contact us at mirror[@]dogado.de.

![]()

seqcomp implements anytime-valid tools for the

sequential comparison of probabilistic forecasters, following the

framework of Choe and Ramdas (2024). Given two competing forecasters and

a sequence of binary or categorical outcomes, the package constructs

confidence sequences and e-processes for the running mean score

difference that are valid simultaneously at every point in time, without

requiring a pre-specified sample size or adjustment for repeated

monitoring.

The package provides:

All boundary computations (normal mixture, gamma-exponential mixture,

polynomial stitching) are implemented from scratch, with no dependency

on the confseq package.

The development version can be installed from GitHub:

# install.packages("pak")

pak::pak("alasgarliakbar/seqcomp")After CRAN acceptance:

install.packages("seqcomp")compare_forecasts() is the main entry point. It computes

pointwise scores, the running mean score difference, a confidence

sequence, and two one-sided e-processes in a single call.

library(seqcomp)

set.seed(1)

n <- 300

y <- rbinom(n, size = 1, prob = 0.55)

# Forecaster p has some signal; forecaster q always predicts 0.5

p <- ifelse(y == 1, 0.62, 0.38)

q <- rep(0.50, n)

out <- compare_forecasts(

p = p,

q = q,

y = y,

scoring_rule = "brier"

)

tail(out[, c("t", "estimate", "lower", "upper", "e_pq", "e_qp")])

#> t estimate lower upper e_pq e_qp

#> 295 295 0.1056 0.07129320 0.1399068 2681618 2.220446e-16

#> 296 296 0.1056 0.07140910 0.1397909 2824574 2.220446e-16

#> 297 297 0.1056 0.07152422 0.1396758 2975161 2.220446e-16

#> 298 298 0.1056 0.07163857 0.1395614 3133784 2.220446e-16

#> 299 299 0.1056 0.07175215 0.1394478 3300873 2.220446e-16

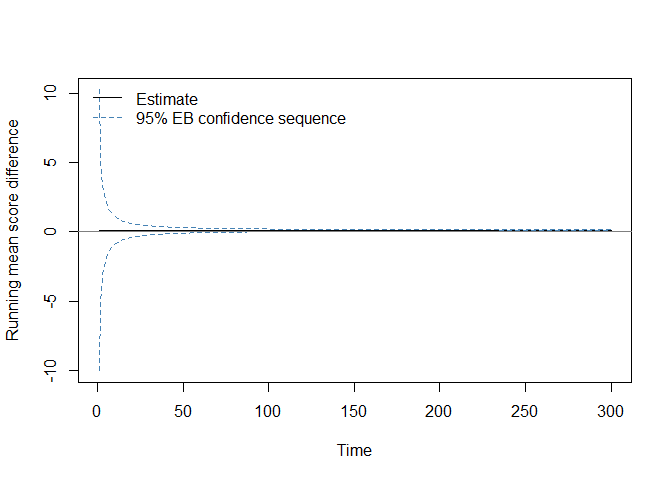

#> 300 300 0.1056 0.07186498 0.1393350 3476882 2.220446e-16The column estimate is the running mean score difference

\(\hat{\Delta}_t = t^{-1}\sum_{i=1}^t (S(p_i,

y_i) - S(q_i, y_i))\). Positive values favour p;

negative values favour q. The columns lower

and upper are the empirical Bernstein confidence sequence

bounds. The columns e_pq and e_qp are the two

one-sided e-process values; the two-sided rejection threshold at level

alpha = 0.05 is 2 / 0.05 = 40.

plot(

out$t, out$estimate,

type = "l",

ylim = range(c(out$lower, out$upper, 0), finite = TRUE),

xlab = "Time",

ylab = "Running mean score difference"

)

lines(out$t, out$lower, lty = 2, col = "steelblue")

lines(out$t, out$upper, lty = 2, col = "steelblue")

abline(h = 0, col = "gray50")

legend(

"topleft",

legend = c("Estimate", "95% EB confidence sequence"),

lty = c(1, 2),

col = c("black", "steelblue"),

bty = "n"

)

Two scale conventions are used throughout, following Choe and Ramdas

(2024) exactly. Theorem 1 (Hoeffding CS) requires \(|\hat{\delta}_i| \leq c\), so

c = 1 is used for Brier or spherical score differences in

\([-1, 1]\). Theorems 2 and 3

(empirical Bernstein CS and e-process) require \(|\hat{\delta}_i| \leq c/2\), so

c = 2 is used for the same score differences.

compare_forecasts() applies these conventions

automatically. They differ from the Python comparecast

package, which applies the Theorem 2/3 convention throughout.

compare_forecasts() is a convenience wrapper. The

underlying functions can be called directly for finer control:

scores_p <- brier_score(p, y)

scores_q <- brier_score(q, y)

cs <- cs_bernstein(scores_p, scores_q, alpha = 0.05, c = 2)

ep <- eprocess(scores_p, scores_q, alpha = 0.05, c = 2)The statistical methods in seqcomp are based on:

The package was developed as part of a bachelor’s thesis at the Vienna University of Economics and Business (WU Vienna).

If this package is used in published work, please cite the package itself and the following papers:

citation("seqcomp")Choe, Y. J. and Ramdas, A. (2024). Comparing Sequential Forecasters. Operations Research, 72(4), 1368–1387. https://doi.org/10.1287/opre.2021.0792

Howard, S. R., Ramdas, A., McAuliffe, J. and Sekhon, J. (2021). Time-uniform, nonparametric, nonasymptotic confidence sequences. The Annals of Statistics, 49(2). https://doi.org/10.1214/20-AOS1991

Howard, S. R., Ramdas, A., McAuliffe, J. and Sekhon, J. (2020). Time-uniform Chernoff bounds via nonnegative supermartingales. Probability Surveys, 17, 257–317. https://doi.org/10.1214/18-PS321

Ramdas, A., Grünwald, P., Vovk, V. and Shafer, G. (2023). Game-theoretic statistics and safe anytime-valid inference. Statistical Science, 38(4), 576–601. https://doi.org/10.1214/23-STS894

Waudby-Smith, I., Arbour, D., Sinha, R., Kennedy, E. H. and Ramdas, A. (2024). Time-uniform central limit theory and asymptotic confidence sequences. The Annals of Statistics, 52(6). https://doi.org/10.1214/24-AOS2408

These binaries (installable software) and packages are in development.

They may not be fully stable and should be used with caution. We make no claims about them.

Health stats visible at Monitor.