The hardware and bandwidth for this mirror is donated by dogado GmbH, the Webhosting and Full Service-Cloud Provider. Check out our Wordpress Tutorial.

If you wish to report a bug, or if you are interested in having us mirror your free-software or open-source project, please feel free to contact us at mirror[@]dogado.de.

Robust estimation methods for the mean vector, scatter matrix, and covariance matrix (if it exists) from data (possibly containing NAs) under multivariate heavy-tailed distributions such as angular Gaussian (via Tyler’s method), Cauchy, and Student’s t distributions. Additionally, a factor model structure can be specified for the covariance matrix. The latest revision also includes the multivariate skewed t distribution.

The package can be installed from CRAN or GitHub:

# install stable version from CRAN

install.packages("fitHeavyTail")

# install development version from GitHub

devtools::install_github("convexfi/fitHeavyTail")To get help:

library(fitHeavyTail)

help(package = "fitHeavyTail")

?fit_mvtTo cite fitHeavyTail

in publications:

citation("fitHeavyTail")To illustrate the simple usage of the package fitHeavyTail,

let’s start by generating some multivariate data under a Student’s \(t\) distribution with significant heavy

tails (degrees of freedom \(\nu=4\)):

library(mvtnorm) # package for multivariate t distribution

N <- 10 # number of variables

T <- 80 # number of observations

nu <- 4 # degrees of freedom for heavy tails

set.seed(42)

mu <- rep(0, N)

U <- t(rmvnorm(n = round(0.3*N), sigma = 0.1*diag(N)))

Sigma_cov <- U %*% t(U) + diag(N) # covariance matrix with factor model structure

Sigma_scatter <- (nu-2)/nu * Sigma_cov

X <- rmvt(n = T, delta = mu, sigma = Sigma_scatter, df = nu) # generate dataWe can first estimate the mean vector and covariance matrix via the traditional sample estimates (i.e., sample mean and sample covariance matrix):

mu_sm <- colMeans(X)

Sigma_scm <- cov(X)Then we can compute the robust estimates via the package fitHeavyTail:

library(fitHeavyTail)

fitted <- fit_mvt(X)We can now compute the estimation errors and see the significant improvement:

sum((mu_sm - mu)^2)

#> [1] 0.2857323

sum((fitted$mu - mu)^2)

#> [1] 0.1487845

sum((Sigma_scm - Sigma_cov)^2)

#> [1] 5.861138

sum((fitted$cov - Sigma_cov)^2)

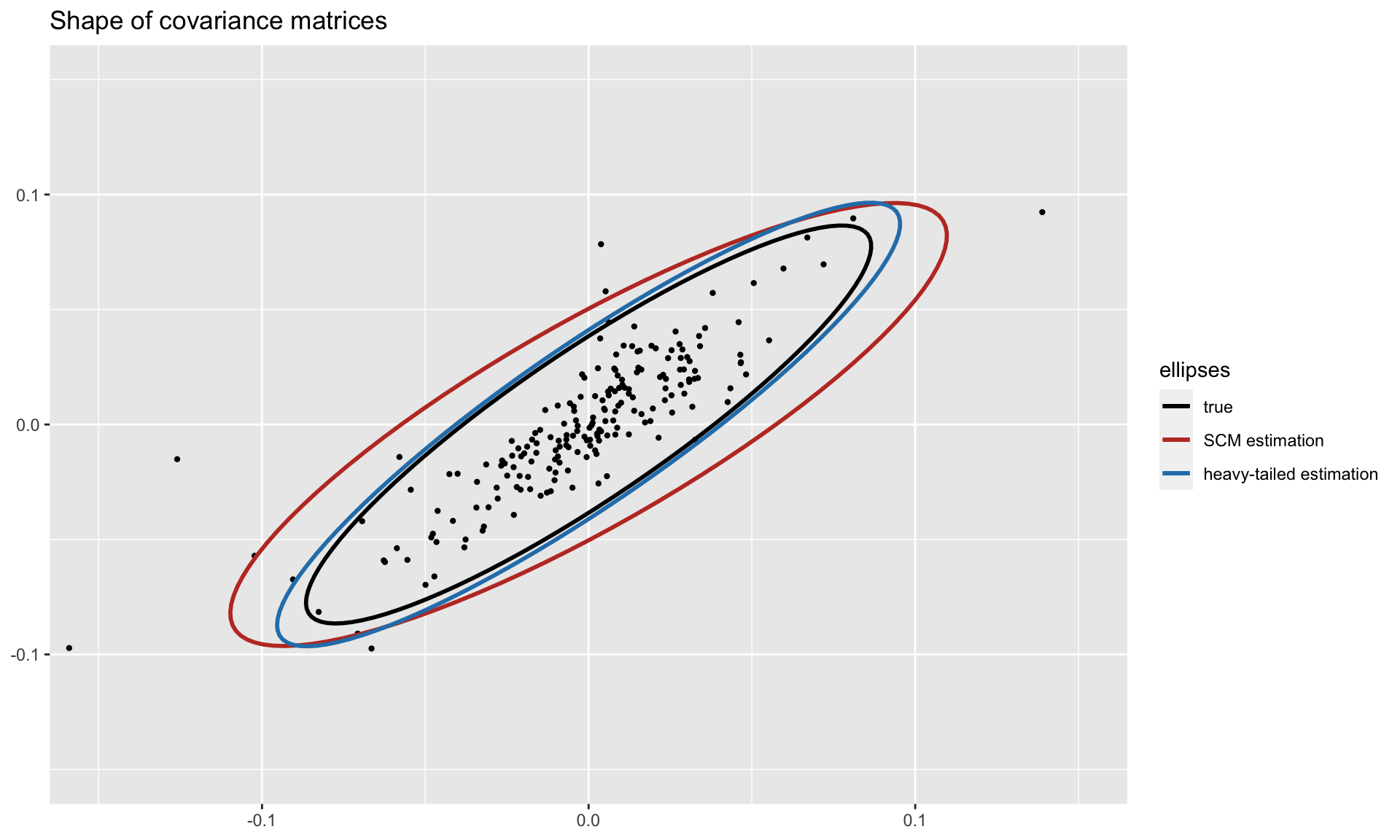

#> [1] 4.663539To get a visual idea of the robustness, we can plot the shapes of the covariance matrices (true and estimated ones) on two dimensions. Observe how the heavy-tailed estimation follows the true one more closely than the sample covariance matrix:

For more detailed information, please check the vignette.

README file: GitHub-readme.

Vignette: CRAN-vignette and GitHub-vignette.

These binaries (installable software) and packages are in development.

They may not be fully stable and should be used with caution. We make no claims about them.

Health stats visible at Monitor.